Russian Lubricants Market Size and Share Analysis – Growth Trends and Forecast to 2022

The lubricants market value reached $120.21 billion in 2022 and will reach $176.25 billion by 2030, registering a CAGR of 3.1% for the forecast period 2023-2030.

In this analysis, the Russian lubricants market is segmented by end user (Automotive, Heavy Equipment, Metallurgy & Metalworking, Power Generation)

Russian Lubricants Market Analysis

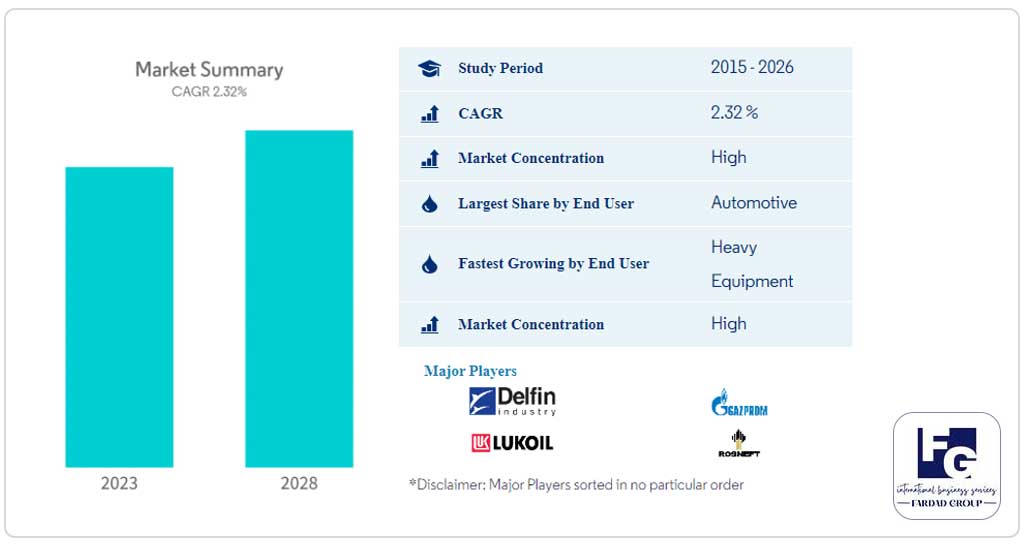

The Russian lubricants market reached 1.19 billion liters in 2021 and is projected to register a CAGR of 2.32% to reach 1.34 billion liters by 2026.

Largest End-User Segment – Automotive: Owing to the huge volume of engine and gear oils used in motor vehicles compared to other industrial applications, automotive was the largest end-user among all categories.

Fastest Growing End-User Segment – Heavy Equipment: Owing to the increasing use of machinery in sectors such as mining, construction, and agriculture, heavy equipment is the fastest growing end-user of lubricants in the country.

Largest Segment by Product Type – Engine Oil: Engine oil is the most widely consumed product type in Russia due to the high volume of engine oil and high change frequency required to lubricate IC engines.

Fastest Segment by Product Type – Gear & Transmission Oils: Gear & Transmission Oils are expected to grow faster than any other product segment, as the use of automatic vehicles and industrial rebounders increases.

Russian Lubricants Industry Segmentation (By User)

Automotive

Heavy Equipment

Metallurgy & Metalworking

Power Generation Other End-User Industries

Russian Lubricants Market Trends

This section covers the key market trends shaping the Russian lubricants market according to our research experts:

Largest Segment by End-User: Automotive

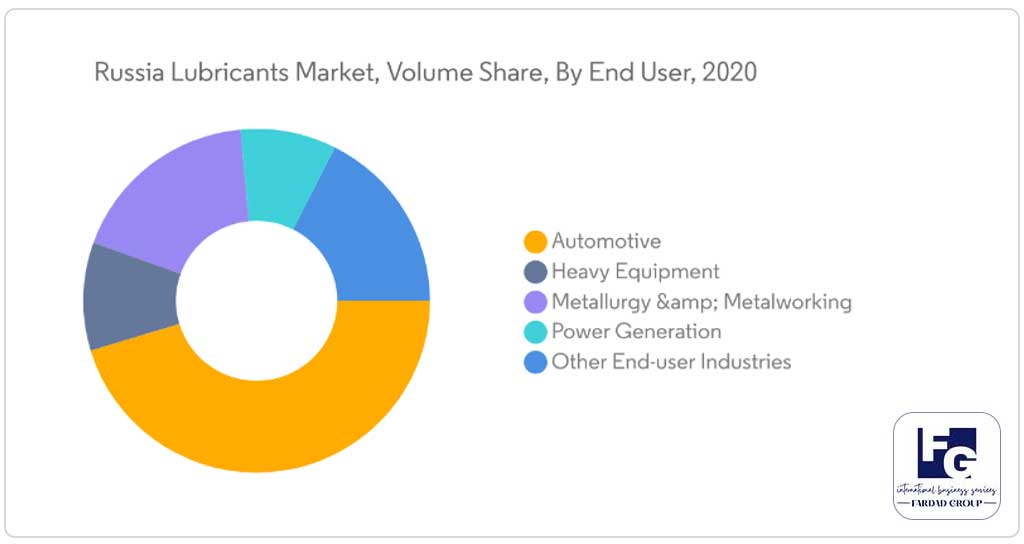

In 2020, the automotive industry dominated the Russian lubricants market, accounting for over 45% of the total oil consumption in the country. During 2015-2019, lubricant consumption in the automotive sector witnessed gradual growth.

In 2020, COVID-19-related restrictions led to a reduction in maintenance requirements from several industries. The automotive industry saw the biggest impact, registering a decline of 15.7% during the year, followed by heavy equipment (11.4%).

Heavy equipment is likely to be the fastest growing end-user industry in the Russian lubricants market during 2021-2026, with a CAGR of 2.94%, followed by automotive (2.31%). The expected recovery in investments and completion of construction and mining projects, coupled with an anticipated increase in commercial vehicle sales, is likely to drive market growth.

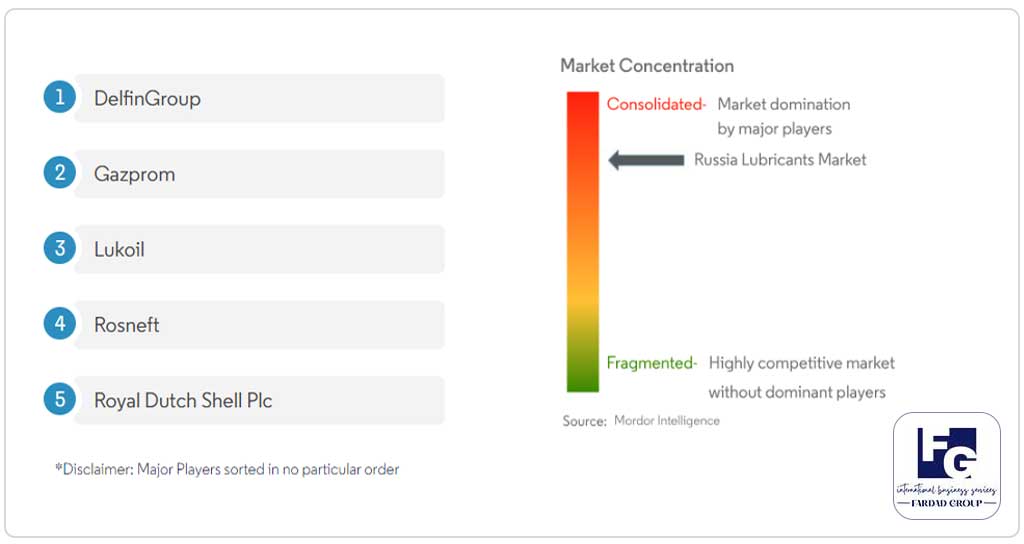

The Russian lubricants market is relatively consolidated, with the top five companies accounting for 73.51%. The main players in this market are Dolphin Group, Gazprom, Lukoil, Rosneft, and Royal Dutch Shell (in alphabetical order).

Over the past 20 years, the Russian automotive market has gone through peaks and troughs in distinct four-year cycles. Excluding off-highway vehicles, there were 52 million vehicles in Russia at the beginning of 2019, of which 81 percent were passenger cars, 8 percent were light commercial vehicles, 7 percent were heavy commercial vehicles, and 4 percent were motorcycles. More than three million vehicles are produced in Russia annually. Russia has vast reserves of oil and natural gas, but US-led sanctions have prevented them from being fully exploited, delaying the growth of the industry because it requires significant investment.

Since 2016, Russian imports of lubricants for vehicles and transportation have remained largely stable, with recent growth of about 270 kilotonnes per year. Mobil, Castrol, ZIC, Total Elf, LiquiMoly, and others are available. Shell also imports various base oils and finished goods. Most lubricant additives are imported, leaving local companies such as Qualitet and Naftan Refinery Lukoil with a limited range of products and technological capabilities. The strong Russian automotive industry is expected to fuel the expansion of this segment.

Competitive Outlook

The top market players hold a healthy share of the Russian lubricants market share. In December 2021, ExxonMobil acquired Garvey to help develop its industrial process automation capabilities.

The major players in the Russian lubricants market include BP PLC (Castrol), DelfinGroup, ExxonMobil Corporation, FUCHS, Gazpromneft – Lubricants, Ltd., Liqui Moly, Lukoil, Obninskorgsintez (SINTEC GROUP), Royal Dutch Shell Plc, and Rosneft.

Gazpromneft – Lubricants, Ltd.

Overview: A global energy company with majority state ownership in Russia is called Gazprom. The business started as a gas distributor in the northwest of England. It was first known as Pennine Gas and then Gazprom Energy and is currently known as SEFE Energy. Its name was changed to SEFE Energy on July 29, 2022. Since April 4, 2022, SEFE and its subsidiaries have been under the control of the German regulatory body, the Bundesnetzagentur (BNetzA). It provides the energy needed by more than 50,000 businesses to continue to provide goods and services used by millions of people in the UK, France and the Netherlands.

Product portfolio: Modern engine and transmission oils, greases, antifreeze and fluids for cars and light commercial vehicles are covered under the Gazprom Neft brand. Gazpromneft-Lubricants produces engine oils under the premium brand G-Energy at its facility in Bari, Italy.

Key development: The marine lubricants contract between Gazpromneft-Lubricants and the FESCO FESCO shipping group was extended on March 20, 2021. Following the terms of the contract, Gazpromneft-Lubricants will deliver engine, gear, compressor, turbine oils, lubricants and technical fluids to the FESCO fleet.

Key and important factors for the presence of Iranian manufacturers in the Russian market

According to the initial research conducted on the industrial lubricants industry in the large Russian market and considering the key factors:

High and consistent quality of manufactured products

Preferential tariffs on import duties of Iranian goods to Russia

Low export costs of Iranian products to Russia compared to Western and Chinese goods

The proximity and proximity of Iran and Russia as a logistical advantage and the possibility of exporting Iranian goods to Russia by various methods such as land, rail and sea transportation in the shortest time and at low shipping prices

The absence of a large part of the market from famous Western brands

The possibility of rapidly expanding market share and access to the competitive and trade space in Russia

It can be said that there is a high economic justification for entering the large Russian-Eurasian market, and the Fardad Group of Companies is proud to establish effective and successful joint cooperation in this direction.