The Russian adhesives market is expected to register a CAGR of 7.02% by the end of 2023.

Packaging is the largest adhesives consumer industry in Russia. In the Russian adhesives market, packaging is the dominant end-user industry due to its wide range of adhesive applications, including labels, tapes, carton sealing and bonding, and lamination.

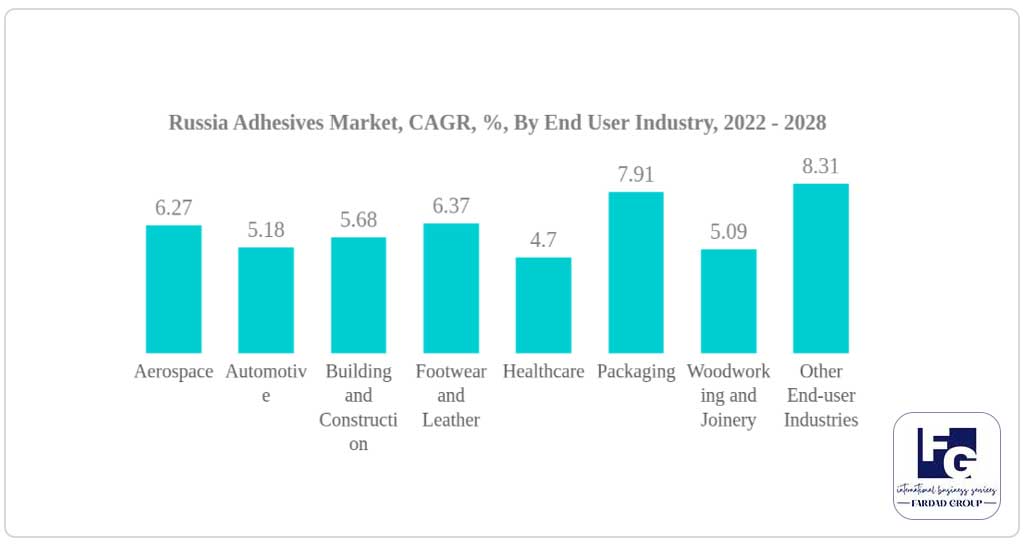

The packaging industry is expected to be the fastest growing end-user industry segment in the Russian adhesives market due to the increasing demand for paper and cardboard packaging and plastic packaging.

Water transfer is the largest technology. Water technology, an environmentally friendly and economically viable solution, holds a major share in the market due to its well-known use in food packaging through emulsion and dispersion systems.

Acrylic-based adhesives hold a major share in the Russian adhesives market due to pressure-sensitive applications in the packaging, construction, and healthcare industries.

Russian Adhesives Consumer Industry Segmentation

Aerospace, Automotive, Building & Construction, Footwear & Leather, Healthcare, Packaging, Woodworking & Joinery are covered as segments by end-user industry. Hot melt adhesives, reactive, solvent, UV cured adhesives, waterborne are covered as segments by technology. Acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA are covered as segments by resin.

Russian Adhesives Market Trends

This section covers the key market trends shaping the Russian adhesives market according to our research experts:

In Russia, polyurethane adhesives, acrylic adhesives, silicone adhesives, and epoxy adhesives are more widely available and are mainly supplied to the packaging, construction, automotive, healthcare, electronics, and other industries. Among all these resin-based adhesives, polyurethane holds the largest share with around 21.8%, followed by silicone, acrylic, and epoxy across the country.

Russia is the eighth largest market for packaged food products in the world with a trade volume of 27.5 million tons. Potato and vegetable processing, coupled with increasing production of beverages (alcoholic and soft), is driving the packaging industry, leading to an increase in demand for adhesives in the coming years. Recent import restrictions by several countries and the import substitution policy of the Russian government are likely to expand opportunities for the packaging industry and simultaneously impact the adhesives market during the forecast period. Water-based adhesives are widely used in the industry due to their cheaper price and high bonding strength required in these applications.

The Russian President announced his decision to build 13 new projects, ranging from education and healthcare to infrastructure development. He instructed the government to increase the country’s economic growth by 2025 relative to the global average. Such projects are expected to help the country achieve sustainable growth and stimulate construction activities during the forecast period. The area of new floors, including residential and non-residential construction in the country, is expected to reach 2 billion square meters by 2028. The increase in construction activities is expected to increase the demand for adhesives in Russia during the forecast period.

Russian Adhesives Industry Overview

The Russian adhesives market is fragmented, with the top five companies accounting for 16.55%. The main players in this market are

Arkema Group

Henkel AG & Co

KGaA

MAPEI S.p.A

RusTA LLC

Sika AG

Cyanoacrylate Adhesives Market – Growth, Trends, COVID-19 Impact and Forecasts (2022-2027)

In 2022, Russian companies produced 14,309 tons of adhesives of animal origin, which is 17.4% less than the results of 2021. The average annual decrease in the production of adhesives of animal origin (CAGR) for the period 2017-2022 was 3%. The leading federal district of the Russian Federation in the production of adhesives of animal origin is the Volga Federal District (59.9% of production for the period 2017-2022), followed by the Southern Federal District (19.1% of production). The production of adhesives of animal origin in June 2023 amounted to 1021.3 tons, a decrease of 44.5% compared to June last year.

The largest adhesive manufacturers in Russia are:

CJSC “MAPEI”

JSC “KIILTO-CLEY”

LLC “ERGOTECH”

OOO “MUREKSIN”

LLC “DAVOS-TRADING”

OOO “POLIDIS”

Analysis of the Russian silicone market

Over the past few years, the Russian silicone market has shown a certain growth trend. For example, in 2022, 11493.9 tons of products were produced, which is an increase of 11% compared to the previous period.

The main volume of production is by the Central Federal District – 74%

Russian manufacturers:

PJSC KHIMPROM

CJSC NMG – POLICOM

JSC ALTAI KHIMPROM

LLC SOFEKS SILIKON

LLC PENTA – 91

OOO PF TECHNOSILOXANES

OOO NPF EMAL

Foreign suppliers:

WACKER CHEMIE AG The largest volume of ELASTOSIL in primary forms was supplied to EUROCHEMICALS s.r.o.

MOMENTIVE PERFORMANCE MATERIALS GMBH

DOW EUROPE GMBH

DONGJUE SILICONE (NANJING) CO.,LTD

NTER-HARZ GMBH

EVONIK RESOURCE EFFICIENCY GMBH

NETLOG GLOBAL FORWARDING TASIMACILIK AS

Import and export figures

Analysis of silicon imports and exports in Russia was conducted by ACG. The volume of imports of finished products for 2022 was 25.50 thousand tons in terms of mass and $111.96 million in terms of money. They mainly imported silicones in primary forms. The main contracts during this period were concluded with Germany – 37%, China – 20%, the USA – 8%, Belgium – 6%. The products were mainly shipped to Moscow – 52%, the Moscow region – 9%, St. Petersburg – 9%, the Krasnodar Territory – 3%.

Analysis of the silicone market showed that exports were carried out to Kazakhstan, Belarus, the Czech Republic, China and Turkmenistan. The regional structure of exports was as follows: Moscow and the suburbs, Vladimir region, St. Petersburg, Novosibirsk. In general, the volume of exports last year was 17 tons. The main exporter was OOO TMK SILMA.

Problems caused by sanctions

This segment of the market in Russia has its own problems. With the imposition of sanctions and the conduct of well-known events, the supply of some formulas and basic materials has ceased. For example, some compounds are purchased only in the USA and have no analogues in the Russian Federation. There is now a real shortage of this product in some applications. For example, in the construction industry, silicone was widely used in the form of adhesives, lubricants, sealants, paints and varnishes. Naturally, such a situation either leads to an increase in the price of products or their disappearance altogether.

Silicon mining companies

West Siberian Electrometallurgical Plant

Chelyabinsk Electrometallurgical Plant

Silicon

Key and important factors for the presence of Iranian manufacturers in the Russian market

According to the initial research conducted on the battery industry in the large Russian market and considering the key factors:

High and consistent quality of Iranian products

Preferential tariffs on import duties of Iranian goods to Russia

Low export costs of Iranian products to Russia compared to Western and Chinese goods

The proximity and proximity of Iran and Russia as a logistical advantage and the possibility of exporting Iranian goods to Russia by various methods such as land, rail and sea transportation in the shortest time and at low shipping prices

The absence of a large part of the market from famous Western brands

The possibility of rapidly expanding market share and access to the competitive and trade space in Russia

It can be said that there is a high economic justification for entering the large Russian-Eurasian market, and the Fardad Group of Companies is proud to establish effective and successful joint cooperation in this direction.